Energy / Iran -- Some Thoughts

The closure of the Strait of Hormuz due to Iranian drone attacks has created a brutal chokepoint for the global economy. About 20 million barrels per day (bpd) of oil flows through there, representing roughly 20% of global oil consumption. The Strait is also the primary export route for the oil producing countries – Saudi Arabia, Iraq, the United Arab Emirates, Kuwait, Qatar, and Bahrain – that hold most of the world’s spare capacity (about 3.5 to 4.0 million barrels per day).

And it’s not just oil. About 20% of global liquified natural gas (LNG) exports also goes through Hormuz (mostly from Qatar). Europe, Japan, and South Korea are heavily dependent on LNG for power generation, and spiking gas prices (if sustained) would be particularly damaging to their economies.

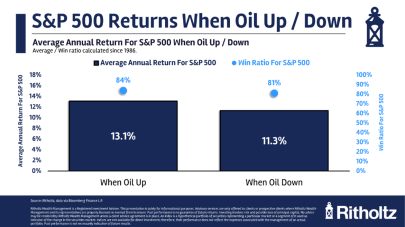

What might be the impact on financial markets? Surprisingly, there’s historically been a positive correlation between oil prices and stocks. That is, rising oil prices tend to be correlated with above-average stock returns ( https://awealthofcommonsense.com/2026/03/how-do-higher-oil-prices-impact-stock-market-returns/ )

Stocks typically do well when oil prices increase because higher energy costs often indicate strong underlying demand from rising economic growth. Obviously, that’s not the case today, as the rapid rise in the price of oil over the last week is due to a lower supply from the war in Iran and the closing of the Strait of Hormuz. So the more critical question is how financial markets have performed in response to supply shocks rather than strong demand. And the answer is that it all depends on how long the shock lasts.

Large cuts in supply, if sustained, have historically led to U.S. recessions. Short-term spikes, like the one that occurred when Russia invaded Ukraine in 2022, tend not to impact the economy much. In fact, although Russia’s invasion of Ukraine at one point pushed up oil by $45 a barrel, a Federal Reserve report found that U.S. GDP growth was only reduced by 0.13% while headline inflation rose just 0.5%.

On the other hand, the U.S. economy is now far more insulated from energy shocks than it was even 20 years ago. As the Wall Street Journal recently reported https://www.wsj.com/economy/why-the-oil-shock-probably-wont-derail-the-economy-and-one-way-it-might-c8603382:

“The U.S. consumed 4% less gasoline in 2025 than in 2007, while producing 42% more goods and services (as measured by gross domestic product, adjusted for inflation). The share of households’ consumption of energy, including electricity, natural gas and gasoline, fell from 5.7% in 2007 to 3.7% last year. Meanwhile, the shale revolution has turned the U.S. into a net exporter of petroleum and major exporter of liquefied natural gas. That means the hit to consumers is offset by a boost to producers.” [U.S. oil production is up 145% since 2003 to 13.7 million bpd, while oil imports from the Gulf have fallen from 3 million bpd to just 500,000 bpd.]

Moreover, the financial markets do seem to be betting that the war won’t last too long and the Strait of Hormuz will soon be open. Specifically, last week oil prices posted their biggest jump since 1983 (up 36%), but energy stocks were basically flat while ExxonMobil’s stock actually fell slightly. The S&P 500 overall was only down about 2%.

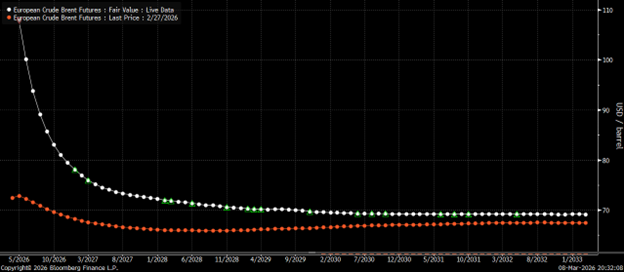

The oil futures curve is telling a similar story.

The white line shows the oil futures curve today (red is where it was before the war). As you can see, oil traders expect prices to fall substantially and in fairly short order. Let’s hope they’re right.